Segmented business results

According to the General Statistics Office, Vietnam's total import-export turnover in the first half of 2025 reached USD 432.03 billion, up 16.1% year-on-year. Key export items such as textiles, footwear, computers, electronic products, and components continued to maintain double-digit growth thanks to rising demand and the “front-loading” effect (early ordering) ahead of reciprocal tariff changes.

In the medium and long term, enterprises are implementing strategies to diversify export markets and increase localization rates to take advantage of signed trade agreements, thereby expanding consumption markets and reducing the impact of U.S. reciprocal tariffs.

As a sector directly affected by trade flows, shipping recorded clear divergence in the first half of 2025: leading players continued to grow, while companies with old fleets saw business performance plunge.

Asian and Asia–Europe routes will become more vibrant as Vietnamese enterprises diversify their export markets to reduce reliance on the U.S. market.

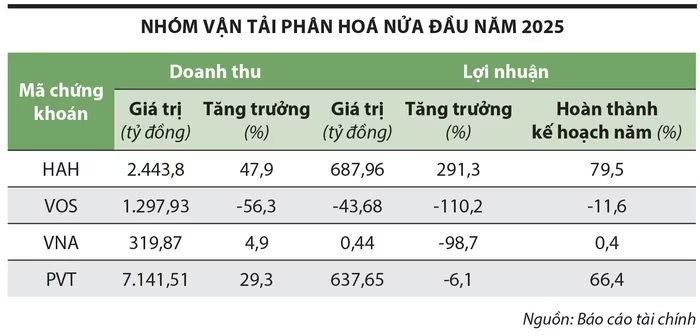

At Hai An Transport & Stevedoring JSC (Hai An, ticker: HAH), in the first half of 2025, revenue rose 47.9% to VND 2,443.8 billion; net profit surged 291.3% to VND 687.96 billion, completing 79.5% of the full-year plan.

In February 2025, Hai An successfully invested in the container vessel Haian Zeta with a capacity of 1,702 TEU, raising its fleet to 17 vessels, mainly operating intra-Asia routes. Specifically, Haian Zeta was time-chartered by Sealead Shipping to operate the Mediterranean–North Africa–U.S. East Coast route; this is Hai An’s first vessel operating to the U.S., opening opportunities for subsequent vessels to run long-haul routes such as the U.S. or Europe.

Previously, Hai An continuously invested and rejuvenated its fleet by acquiring Haian Link and Haian Bell (2018), Haian Mind (2019), Haian East and Haian West (2021), Anbien Bay, Haian City, and A Roku (2022). In 2024, the company received and put into operation four new container ships.

At PetroVietnam Transportation Corporation (PVTrans, ticker: PVT), in the first half of 2025, revenue increased 29.3% to VND 7,141.5 billion; however, net profit decreased 6.1% to VND 637.6 billion, completing 66.4% of the full-year profit target (VND 960 billion).

In contrast, Vietnam Ocean Shipping JSC (Vosco, ticker: VOS) and Vietnam Shipping JSC (Vinaship, ticker: VNA) reported plunging business results. Vosco’s profit before tax recorded a loss of VND 43.7 billion, while Vinaship posted only VND 0.44 billion – down 98.7% year-on-year.

After more than 11 years without new investments, Vinaship unexpectedly acquired the vessel Vinaship Unity at the end of 2024 with a deadweight of 28,189 DWT, raising its fleet to 5 ships with a total tonnage of 100,111 DWT and an average age of 21.5 years. In 2025, the company plans to add two second-hand dry bulk carriers (30,000–35,000 DWT) and dispose of Vinaship Pearl (24,241 DWT).

Similarly, after more than 11 years without new vessel investment, at the end of 2024, Vosco approved a plan to invest in 10 vessels with a maximum total value of USD 414 million, including two second-hand Supramax bulk carriers (56,000–58,000 DWT, under 15 years old); four newly built Ultramax vessels (62,000–66,000 DWT); and four MR product tankers (around 50,000 DWT). This year, Vosco will continue seeking opportunities to invest in or charter suitable vessels, prioritizing Supramax and Ultramax bulk carriers, MR product tankers, chemical tankers, and container ships.

Thus, although both Vinaship and Vosco are ambitious in ramping up investment, their core operations face challenges due to owning older fleets, which risk becoming obsolete and less efficient compared to newer vessels, causing their business results to remain difficult.

With divergent business results, VOS and VNA stocks have moved sideways for more than seven months in 2025. In contrast, HAH stock, despite a strong rise in May thanks to tariff deferral news, quickly leveled off, falling only 1.2% from May 27 to August 19.

Challenges in the second half of the year

Shinhan Vietnam Securities assessed that the new U.S. tariffs are unlikely to trigger another wave of massive cargo shipments in the final months of the year as in early 2025. Average spot freight rates on major routes from the Far East to the U.S. have plummeted, currently at the lowest level since December 2023. At the same time, with little sign of a traditional peak season in Q3, carriers will face overcapacity issues.

“In the long term, the imposition of high tariffs on imports, especially goods from China, may shift global trade flows. We believe Asian and Asia–Europe routes will become more active as domestic enterprises diversify export markets to reduce reliance on the U.S. market,” forecast Shinhan Vietnam Securities.

In fact, the Drewry World Container Index on August 14 dropped 33.7% compared to June 12, from USD 3,543 to USD 2,350 per 40ft container, and down 41% from the beginning of the year. The peak export season shifting from Q3 to Q2 reflects weakening cargo demand, leading to concerns over shipment volumes and affecting shipping enterprises. Therefore, despite a booming stock market, shipping stocks have mostly moved sideways or declined recently.